Understanding Payroll Taxes: A Complete Guide to FICA, Withholding, and Net Pay (2026)

Understanding Payroll Taxes: A Complete Guide to FICA, Withholding, and Net Pay (2026)

You negotiated a salary of $60,000. You divide by 26 pay periods and expect $2,307 every two weeks. You open your bank app on Friday... and see a deposit for $1,750.

Where did the rest of the money go?

Welcome to the world of payroll taxes. According to the IRS, employers are required by law to withhold several types of taxes from every paycheck — and understanding these deductions is crucial for financial literacy. In this guide, we will decode every line item on your pay stub so you know exactly where your money is going, why it's being taken, and how to make sure the math is right.

The Big Two: What's Taken Out of Your Check?

Every paycheck has two main categories of mandatory deductions — taxes you must pay by law:

- FICA Taxes (Social Security & Medicare)

- Income Tax Withholding (Federal & State)

They function very differently from each other. FICA taxes are flat-rate and predictable. Income taxes are progressive and depend on your personal situation. Let's break down each one.

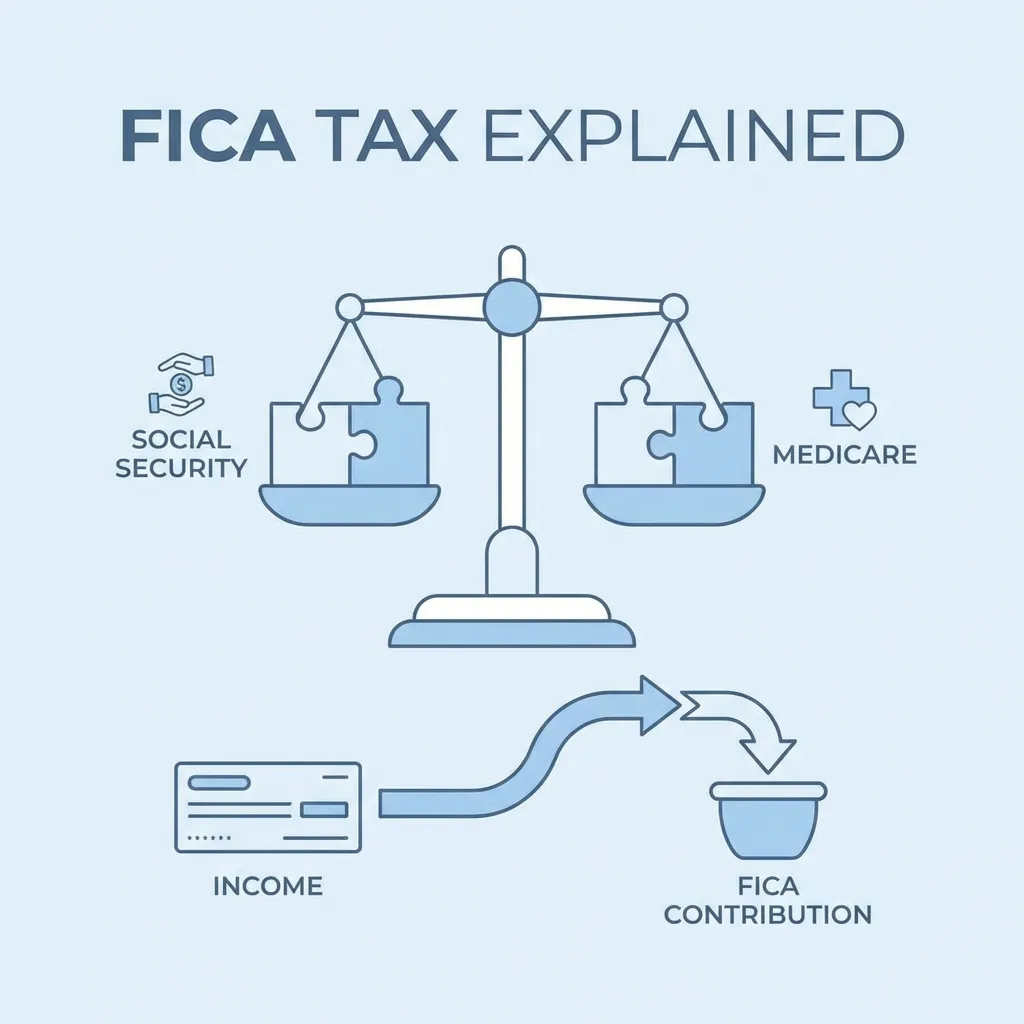

1. FICA Taxes (The Flat Rates)

FICA stands for the Federal Insurance Contributions Act, signed into law in 1935 as part of the Social Security Act. These taxes fund the social safety net programs that support retirees, the disabled, and children of deceased workers. Every working American pays FICA regardless of income level, filing status, or deductions.

Unlike income tax, FICA taxes are (mostly) flat rates — everyone pays the same percentage.

Social Security Tax (OASDI)

- Rate: 6.2% of your Gross Pay

- Purpose: Pays for retirement benefits, disability insurance (SSDI), and survivorship benefits for families of deceased workers

- The Wage Base Limit: In 2026, you only pay this tax on the first $176,100 you earn (SSA announcement). Once your year-to-date earnings exceed that threshold, Social Security withholding stops for the rest of the year

- Employer Match: Your employer also pays a matching 6.2% on your behalf — this doesn't appear on your pay stub but effectively doubles the contribution to Social Security

- Self-employed: If you're self-employed, you pay both halves (12.4%) as "self-employment tax" via Schedule SE

How it appears on your stub: Look for "SS," "OASDI," "Soc Sec," or "Social Security" on your pay stub. See our paystub abbreviations guide for a full glossary.

Medicare Tax (HI)

- Rate: 1.45% of your Gross Pay

- Purpose: Funds Hospital Insurance (Medicare Part A) for seniors and qualified individuals

- The Limit: None. Unlike Social Security, you pay Medicare tax on every dollar you earn — there is no wage base cap

- Additional Medicare Tax: High earners pay an extra 0.9% on earnings over $200,000 (single) or $250,000 (married filing jointly) under the Affordable Care Act

- Self-employed: You pay both halves (2.9%), plus the 0.9% surcharge if applicable

The Combined FICA Math: Together, Social Security (6.2%) and Medicare (1.45%) take 7.65% of your paycheck right off the top. For a $5,000 bi-weekly gross pay, that's $382.50 before income taxes even enter the picture.

Understanding the Wage Base Limit with an Example

If you earn $200,000 per year:

- January through September: Social Security is withheld at 6.2% on every paycheck

- Once your YTD earnings hit $176,100: Social Security withholding stops

- October through December: You'll notice larger paychecks because the 6.2% is no longer being deducted

- Medicare: Continues at 1.45% all year, plus the extra 0.9% kicks in after $200,000

This is why high earners sometimes see their net pay increase later in the year — it's not a raise, it's the Social Security cap being reached.

2. Income Tax Withholding (The Variable Rates)

This is where it gets complicated. Unlike FICA's flat rates, income tax is progressive — meaning the more you earn, the higher the percentage on your top dollars. The U.S. uses a tax bracket system defined in IRS Revenue Procedures.

Federal Income Tax

Federal withholding is essentially a pre-payment of your annual tax bill to the IRS. Your employer calculates the amount to withhold based on:

- Your Earnings: Higher salary = higher marginal tax bracket

- Your W-4 Form: This form (updated in 2020) tells your employer your filing status (Single, Married Filing Jointly, Head of Household) and any adjustments for dependents, additional income, or extra withholding

2026 Federal Tax Brackets (Single Filer):

| Taxable Income | Tax Rate |

|---|---|

| $0 – $11,925 | 10% |

| $11,926 – $48,475 | 12% |

| $48,476 – $103,350 | 22% |

| $103,351 – $197,300 | 24% |

| $197,301 – $250,525 | 32% |

| $250,526 – $626,350 | 35% |

| Over $626,350 | 37% |

Important: These brackets are marginal, not flat. If you earn $60,000, you don't pay 22% on all of it. You pay 10% on the first $11,925, 12% on the next chunk, and 22% only on the amount above $48,475.

2026 Pro Tip: If you consistently get a huge tax refund in April, you are withholding too much. You are essentially giving the government an interest-free loan. Use the IRS Tax Withholding Estimator to adjust your W-4 and get more money in each paycheck.

State Income Tax

State income tax varies wildly depending on where you live and work:

- High Tax States: California (up to 13.3%), New York (up to 10.9%), Hawaii (up to 11%)

- Flat Tax States: Pennsylvania (3.07%), North Carolina (4.5%), Illinois (4.95%) — everyone pays the same rate

- No Income Tax States: Texas, Florida, Nevada, Washington, Wyoming, South Dakota, Tennessee, Alaska, and New Hampshire (wages only)

If you live in a no-income-tax state like Texas or Florida, you'll notice significantly higher take-home pay compared to someone earning the same salary in California or New York. Our state-by-state paystub guide covers the specific requirements for each state.

Local & City Taxes

Some cities and counties add additional taxes on top of state taxes:

- New York City: Up to 3.876% city income tax

- Philadelphia: 3.75% city wage tax for residents

- Detroit: 2.4% city income tax

- Various Ohio cities: 1-3% municipal income tax

These often appear as separate line items on your pay stub, labeled as "City Tax," "Local Tax," or with the specific municipality name.

3. Pre-Tax Deductions (Benefits That Save You Money)

Below the tax lines, you'll see deductions for benefits you enrolled in. Many of these are pre-tax, meaning they reduce your taxable income — saving you money on both income tax and FICA taxes:

Retirement Contributions

- 401(k) / 403(b): Traditional contributions reduce your current taxable income. If you contribute $500 per paycheck and you're in the 22% bracket, you save approximately $110 in taxes per pay period

- Roth 401(k): Contributions are made after-tax — no immediate tax savings, but withdrawals in retirement are tax-free

Health Insurance

- Medical/Dental/Vision Premiums: Your share of employer-sponsored health coverage. According to KFF, the average employee contribution for family coverage is about $6,575/year ($253 per bi-weekly paycheck)

- HSA (Health Savings Account): Pre-tax contributions up to $4,300 (individual) or $8,550 (family) in 2026, usable for qualified medical expenses

- FSA (Flexible Spending Account): Pre-tax contributions up to $3,200 in 2026, but with a "use it or lose it" rule

Why Pre-Tax Matters with a Real Example: If you earn $2,307 bi-weekly and contribute $200 to a 401(k) and $100 to health insurance:

- Taxes are calculated on $2,007 (not $2,307)

- At the 22% federal bracket, you save ~$66 in federal taxes per paycheck

- Plus savings on FICA (7.65%) = another ~$23

- Total tax savings: ~$89 per paycheck, or ~$2,314 per year, just from pre-tax deductions

4. Post-Tax Deductions

Some deductions come out after taxes have been calculated:

- Roth 401(k) / Roth IRA contributions: Taxed now, tax-free in retirement

- Life insurance premiums (over $50,000 in coverage — a taxable fringe benefit)

- Wage garnishments: Court-ordered deductions for child support, student loans, or other debts

- Union dues: Membership fees for labor unions

- After-tax disability insurance

Real World Example: The $60,000 Salary Breakdown

Let's see the math in action for a single filer in a state with a 5% flat income tax, with typical benefits.

Annual Salary: $60,000 | Pay Frequency: Bi-Weekly (26 pay periods)

Gross Pay (Bi-Weekly): $2,307.69

| Deduction | Calculation | Amount |

|---|---|---|

| Social Security | 6.2% of Gross | -$143.08 |

| Medicare | 1.45% of Gross | -$33.46 |

| Federal Withholding | Based on W-4 (Single, 0 adjustments) | -$211.53 |

| State Tax | 5% of taxable income | -$105.38 |

| 401(k) | 5% pre-tax contribution | -$115.38 |

| Health Insurance | Employee share of medical | -$85.00 |

| Dental/Vision | Employee share | -$25.00 |

| TOTAL DEDUCTIONS | -$718.83 |

Net Pay (Your Bank Deposit): $1,588.86

Approximately 31% of your gross pay was deducted — but $200+ of that went into your own retirement and health benefits.

Note: Federal withholding was calculated using IRS Publication 15-T percentage method for a 2026 single filer. Actual amounts vary based on your specific W-4 elections.

Why Accuracy Matters for Self-Generated Pay Stubs

If you are generating your own pay stubs as a freelancer or business owner, getting these numbers right is non-negotiable. Verification professionals check for:

- Wrong FICA rates: If Social Security isn't exactly 6.2% or Medicare isn't 1.45%, lenders will spot the error immediately. This is the #1 indicator of fake pay stubs

- Under-withholding: You'll owe a massive tax bill plus underpayment penalties in April

- Over-withholding: You lose cash flow throughout the year by overpaying the government

- Incorrect YTD totals: Year-to-date figures must accumulate accurately across every pay period

The Easy Way: Automated Calculations

Don't attempt to manually calculate progressive tax brackets, FICA wage bases, and state-specific taxes with a spreadsheet. Use a professional that's updated with the latest 2026 tax laws for federal and all 50 states, automatically calculating the exact penny for:

- Progressive federal tax brackets

- FICA wage base limits and phaseouts

- State-specific taxes including SDI (California), SUI, and local taxes

- Pre-tax deduction effects on taxable income

Frequently Asked Questions

Why is my first paycheck smaller than expected?

Your first paycheck may seem small because tax withholding is calculated as if you earned that rate for the full year, placing you in a higher bracket than your actual partial-year earnings warrant. Additionally, benefit enrollment deductions typically begin with your first check.

Can I change how much tax is withheld?

Yes. Submit a new W-4 form to your employer at any time. You can increase or decrease withholding by adjusting your filing status, claiming dependents, or requesting additional withholding.

Why do I see different Social Security amounts on different stubs?

If your year-to-date earnings approach the wage base limit ($176,100 in 2026), your final Social Security deduction for the year will be smaller — calculated only on the remaining amount below the cap.

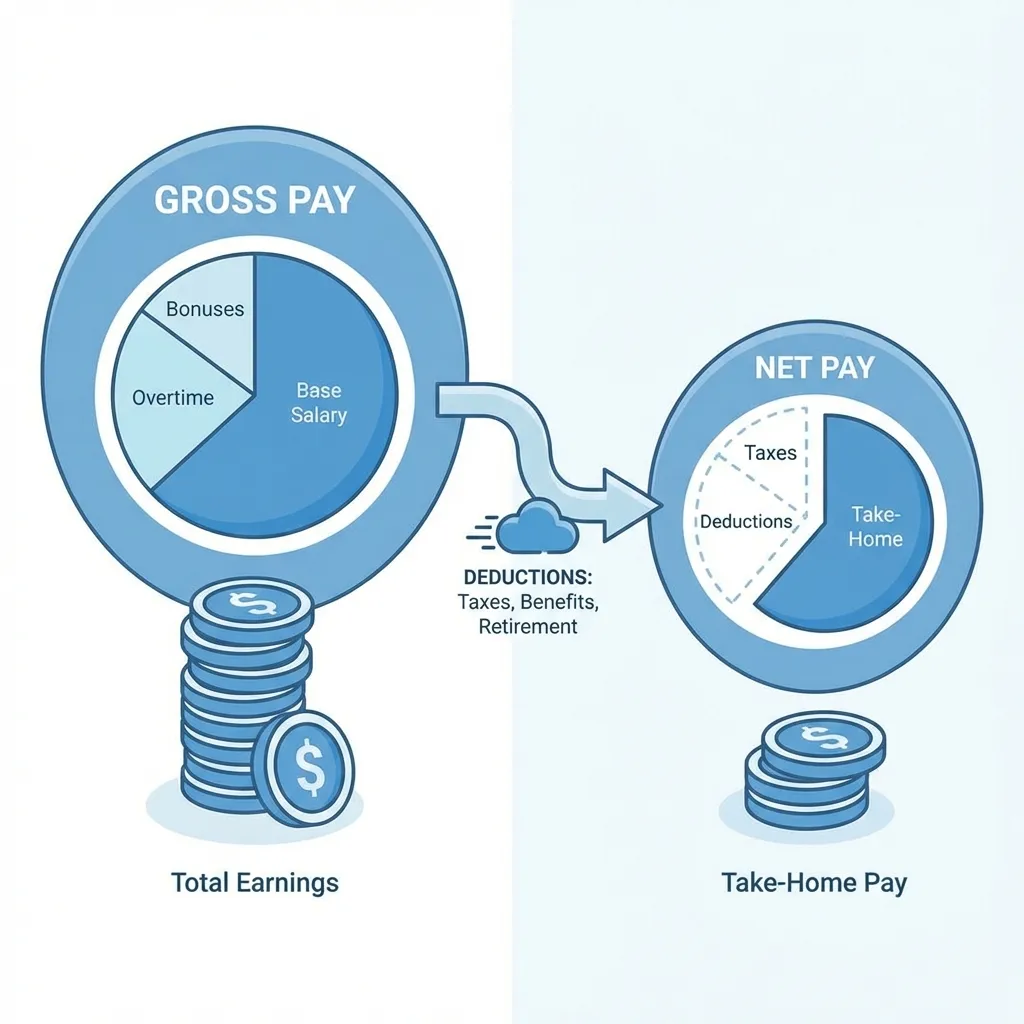

What's the difference between gross pay and net pay?

Gross pay is your total earnings before any deductions. Net pay is what actually hits your bank account after all taxes, insurance premiums, and retirement contributions are subtracted.

Are payroll taxes the same as income taxes?

No. "Payroll taxes" specifically refers to FICA (Social Security + Medicare), which are flat-rate and fund specific social programs. "Income taxes" are progressive and fund general government operations. Both appear on your pay stub but serve different purposes.

How do self-employed people pay payroll taxes?

Self-employed individuals pay both the employee and employer portions of FICA (a combined 15.3%) through the self-employment tax reported on Schedule SE of their tax return.

Conclusion

Taxes are inevitable, but confusion isn't. By understanding every line item on your pay stub — from FICA's flat 7.65% to progressive federal brackets to pre-tax benefit savings — you can catch errors, optimize your W-4 to keep more cash in each paycheck, and plan your financial future with eyes wide open.

Need to see the numbers yourself?

Sources & References

- IRS Publication 15 (Circular E) — Employer's Tax Guide

- IRS Publication 15-T — Federal Income Tax Withholding Methods

- Social Security Administration — Contribution and Benefit Base

- IRS Topic 751 — Social Security and Medicare Withholding Rates

- IRS — Tax Withholding Estimator

- IRS — Understanding Employment Taxes

- IRS — Additional Medicare Tax

- IRS — Self-Employment Tax

- KFF — Employer Health Benefits Survey

About ValidPaystubs Editorial Team

Our editorial team consists of HR professionals and financial writers dedicated to providing accurate, up-to-date information on payroll and income verification.