What is a Pay Stub? Complete Guide to Understanding Your Earnings Statement (2026)

What is a Pay Stub? Complete Guide to Understanding Your Earnings Statement (2026)

Every time you get paid, you receive more than just money in your bank account. You also receive a pay stub — a detailed document that explains exactly where your money goes. Yet, most Americans have never truly understood how to read this critical financial document.

According to a survey by the American Payroll Association, nearly 75% of workers have experienced at least one payroll error in their careers. The only way to catch these mistakes? Understanding your pay stub. In this comprehensive guide, we'll answer the question "what is a pay stub?" and teach you how to decode every line, spot errors, and use this knowledge to your financial advantage.

What is a Pay Stub? Definition and Purpose

A pay stub (also known as a payslip, earnings statement, check stub, or wage statement) is a document that accompanies your paycheck or direct deposit. It provides a complete breakdown of your earnings and all deductions for a specific pay period.

While there is no single federal law mandating pay stubs (the FLSA only requires employers to keep records), most states require employers to provide them. See our state-by-state requirements guide for details.

The Purpose of a Pay Stub

Your pay stub serves multiple critical functions in your financial life:

- Transparency: Shows exactly how your gross pay becomes net pay through taxes and deductions

- Record Keeping: Creates a documented paper trail of your income history

- Proof of Income: Landlords, mortgage lenders, and car dealers use it to verify your earnings

- Tax Preparation: The Year-to-Date (YTD) figures help you prepare for tax season and verify your W-2 accuracy

- Error Detection: Allows you to catch mistakes in hours worked, pay rate, or deduction amounts

- Benefits Tracking: Shows your current benefit elections, retirement contributions, and insurance premiums

Anatomy of a Pay Stub: Breaking Down Every Section

Let's dissect a typical pay stub section by section. Understanding these components will make you financially literate for life.

1. Employee Information

This section contains your personal details:

- Employee Name: Your full legal name as it appears on your W-4

- Employee ID: A unique identifier assigned by your employer's payroll system

- SSN (Last 4): The last four digits of your Social Security Number for identification

- Address: Your mailing address on file with your employer

- Department/Position: Your role or department within the organization

2. Employer Information

Details about the company paying you:

- Company Name: The legal entity name of your employer

- Company Address: The business's physical/mailing address

- EIN: Employer Identification Number — the business's tax ID, used by the IRS for tax reporting

- Phone Number: Company contact information (included in some states)

3. Pay Period Information

This section defines the timeframe and frequency:

- Pay Period Start: The first day of the period you're being paid for

- Pay Period End: The last day of the period

- Pay Date: The actual date your paycheck is issued (usually 3-7 days after period end)

- Check Number: A unique identifier for the payment transaction

Pay Frequency Comparison:

| Frequency | Periods/Year | Common In |

|---|---|---|

| Weekly | 52 | Retail, hourly workers |

| Bi-Weekly | 26 | Most common in the U.S. |

| Semi-Monthly | 24 | Salaried positions |

| Monthly | 12 | Executive, some salaried roles |

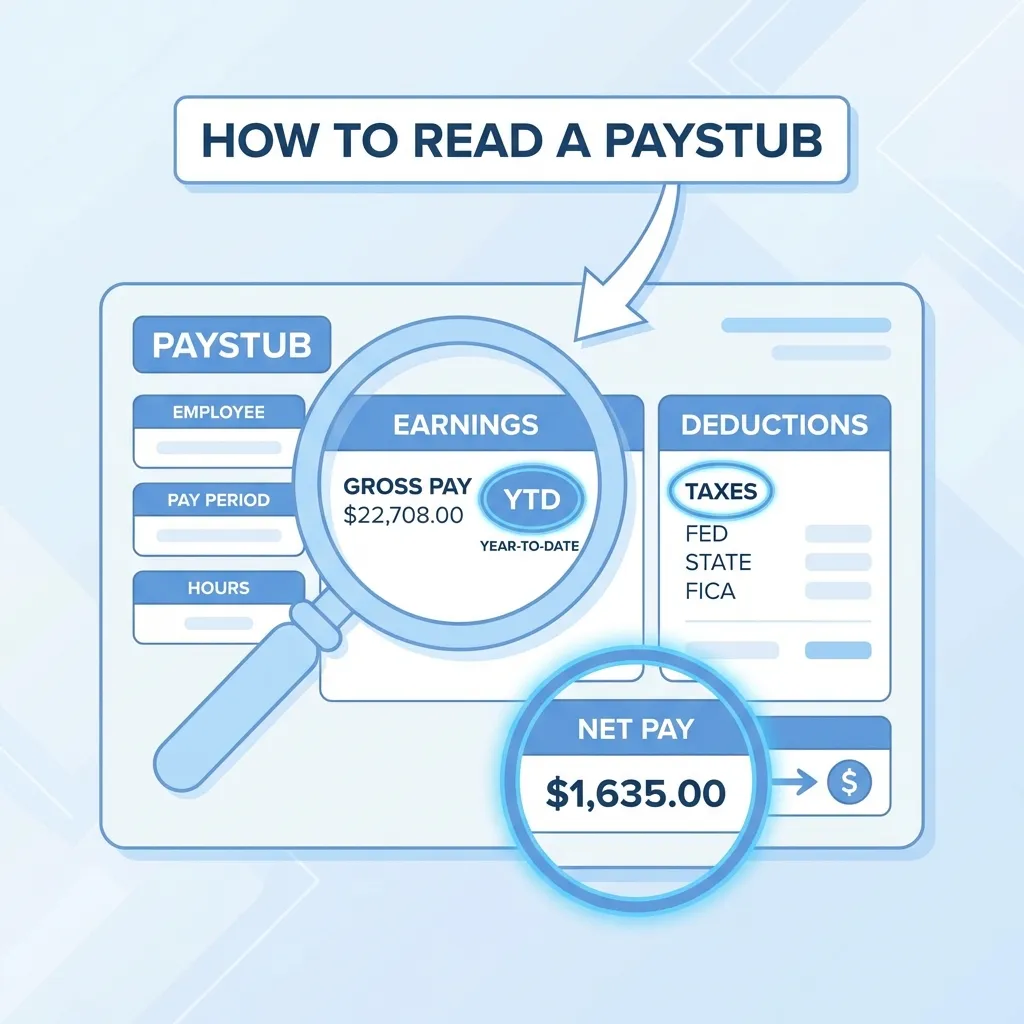

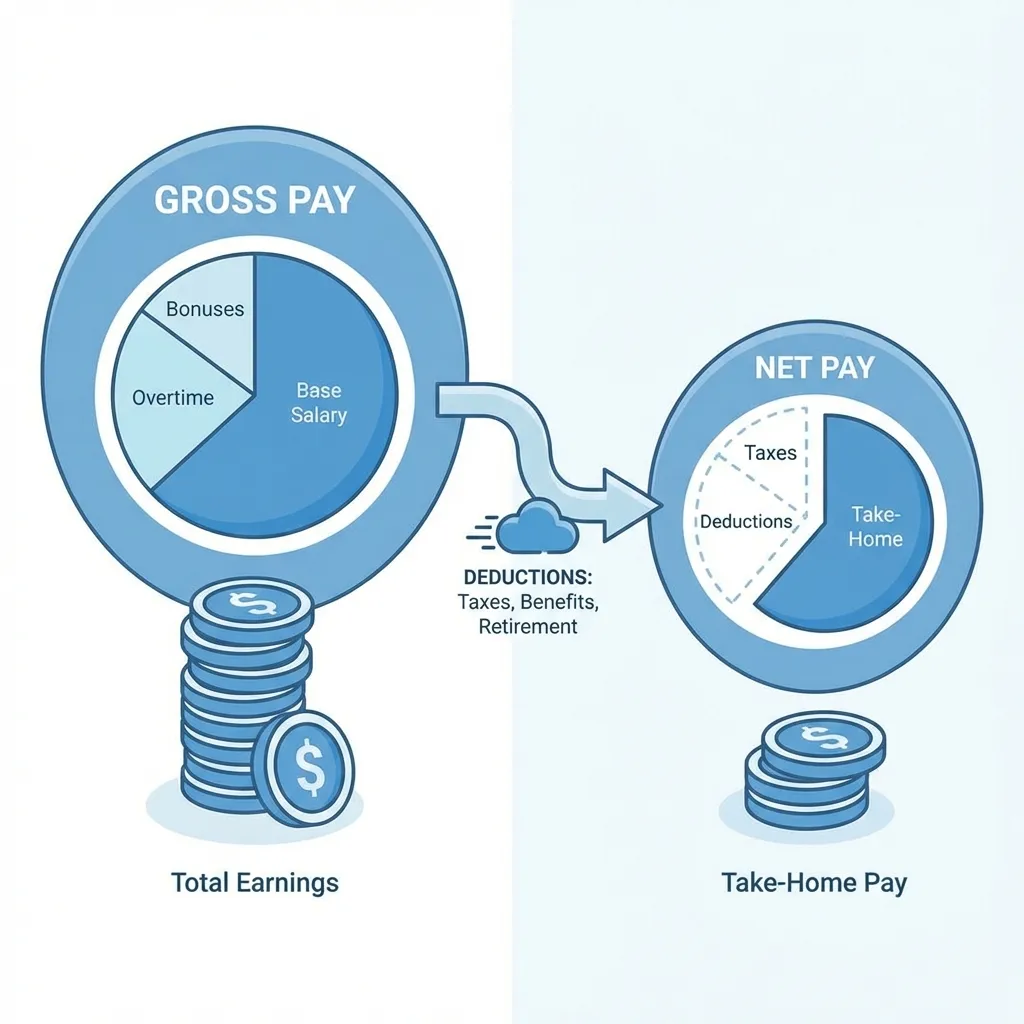

4. Earnings Section (What You Made)

This is the income side of your pay stub:

| Term | What It Means | Example |

|---|---|---|

| Regular Hours | Standard hours at your base rate | 80 hrs × $25 = $2,000 |

| Overtime Hours | Hours over 40/week at 1.5× rate | 5 hrs × $37.50 = $187.50 |

| Double Time | Some states/contracts pay 2× for holidays | 8 hrs × $50 = $400 |

| Holiday Pay | Paid time off for recognized holidays | 8 hrs × $25 = $200 |

| PTO/Vacation | Paid time off used during the period | Varies |

| Commission | Sales-based earnings | Varies |

| Bonus | Performance, signing, or holiday bonuses | Varies |

| Tips | Reported tip income | Varies |

| Gross Pay | Total of all earnings BEFORE deductions | Sum of above |

5. Deductions Section (Where Your Money Goes)

This is where most people get confused. Here's every common deduction and what it means:

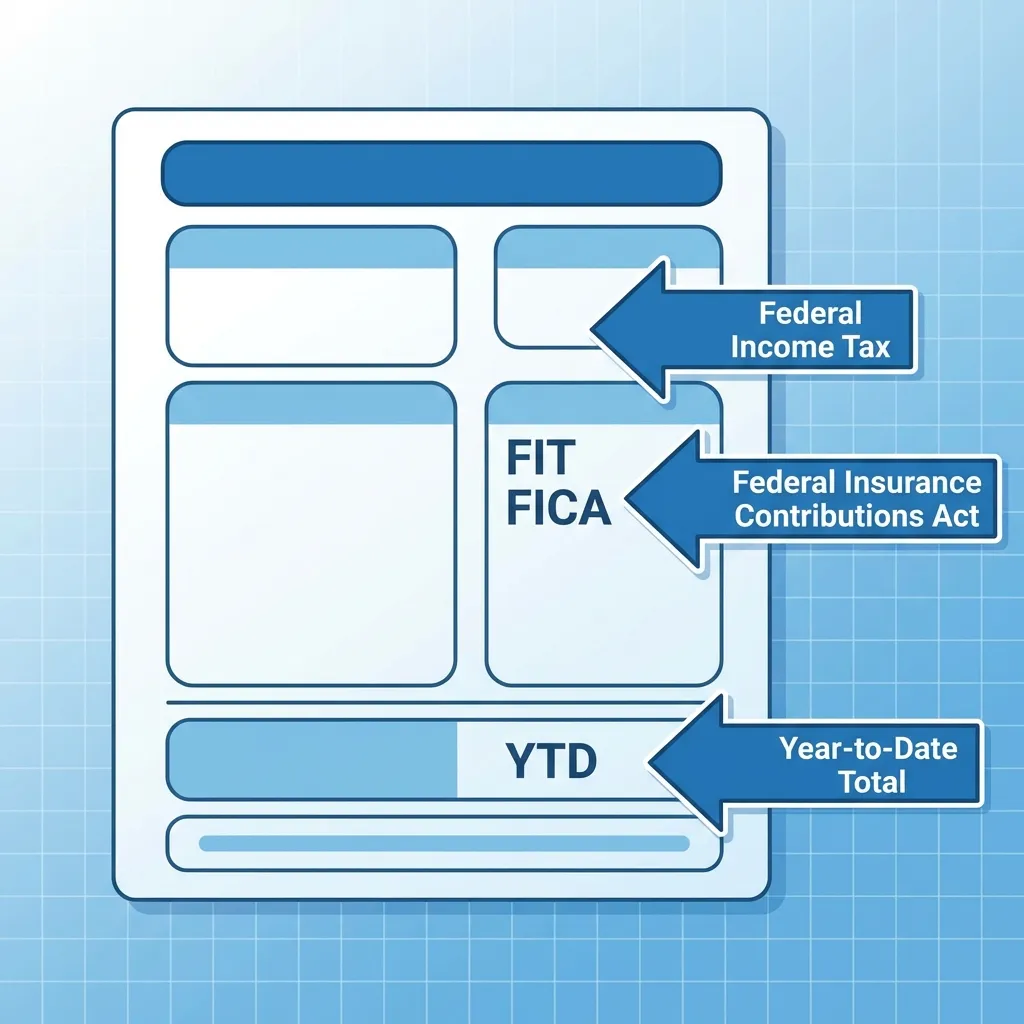

Federal Taxes

| Code on Stub | Full Name | Rate/Amount |

|---|---|---|

| FIT or Fed Tax | Federal Income Tax | 10-37% progressive (IRS brackets) |

| FICA-SS or OASDI | Social Security Tax | 6.2% up to $176,100 |

| FICA-Med or Medicare | Medicare Tax | 1.45%, no cap |

| Add'l Med | Additional Medicare | 0.9% on earnings over $200K |

For a deep dive into FICA, see our FICA Tax Explained guide.

State & Local Taxes

| Code | Full Name | Details |

|---|---|---|

| SIT or State Tax | State Income Tax | 0-13.3% depending on state |

| SDI | State Disability Insurance | Required in CA, NJ, NY, HI, RI |

| SUI | State Unemployment Insurance | Employee portion in some states |

| City Tax or Local | Municipal Tax | NYC, Philadelphia, Detroit, etc. |

Voluntary/Benefit Deductions

| Code | Full Name | Pre-Tax? |

|---|---|---|

| 401(k) or Ret | Retirement contribution | Yes (Traditional) |

| Roth | Roth 401(k) contribution | No |

| Med or Health | Health insurance premium | Yes |

| Dental | Dental insurance premium | Yes |

| Vision | Vision insurance premium | Yes |

| HSA | Health Savings Account | Yes |

| FSA | Flexible Spending Account | Yes |

| Life | Life insurance premium | Partially |

| LTD/STD | Long/Short-term disability | Varies |

| Union | Union dues | No |

| Garn | Wage garnishment | No |

6. Net Pay (Your Take-Home Pay)

Net Pay = Gross Pay - All Deductions

This is the actual amount deposited into your bank account. For most Americans, net pay is approximately 65-80% of gross pay, depending on income, state, and benefit elections.

7. Year-to-Date (YTD) Totals

The YTD column shows cumulative amounts from January 1st through the current pay date. This section is crucial for:

- Tracking annual earnings progress across the year

- Verifying your W-2 accuracy at year-end — your last stub's YTD should closely match your W-2

- Proving income stability to mortgage lenders who check YTD consistency

- Social Security cap tracking — once YTD earnings hit $176,100, SS withholding stops

How to Spot Errors on Your Pay Stub

The American Payroll Association estimates that payroll errors affect 1-8% of paychecks. Here's a checklist for every pay period:

Quick Verification Checks

| What to Check | How to Verify |

|---|---|

| Hours worked | Compare to your personal time records |

| Pay rate | Match against your employment agreement |

| Social Security | Should be exactly 6.2% of gross pay |

| Medicare | Should be exactly 1.45% of gross pay |

| YTD totals | Should equal previous YTD + current period |

| Net pay | Should match your bank deposit amount |

| Benefits deductions | Should match your enrollment elections |

If you find an error, report it to your HR or payroll department immediately in writing. For persistent issues, consult your state labor department.

Why is My Pay Stub Important for Major Life Decisions?

Proof of Income for Housing

When you apply for an apartment or a mortgage, your pay stubs are the primary document reviewers examine. They verify current employment, income level, and financial stability.

Tax Filing and W-2 Verification

Your last pay stub of the year contains YTD totals that should closely match your W-2. If there's a discrepancy, address it with your employer before filing taxes to avoid issues with the IRS.

Legal Proceedings

Pay stubs serve as legal evidence of income in divorce proceedings, child support calculations, workers' compensation claims, and employment disputes.

What if I Don't Receive a Pay Stub?

While not all states require employers to provide pay stubs, most do. If your employer doesn't provide one:

- Check your state's laws using our state requirements guide

- Request in writing from HR — create a documented paper trail

- File a complaint with your state labor board if they refuse

- Create your own if you're self-employed using a professional

How to Create Your Own Pay Stub

If you're a freelancer, contractor, or small business owner, you won't receive a pay stub from anyone — you need to create your own. A professional automatically calculates:

- Federal income tax based on 2026 IRS brackets

- State income tax for all 50 states

- FICA taxes (Social Security + Medicare)

- Net pay after all deductions

- Accurate YTD totals across multiple periods

Frequently Asked Questions

What is a pay stub used for?

A pay stub is used for proof of income (apartments, mortgages, car loans), tax preparation, personal budgeting, and employee records. It provides a detailed breakdown of earnings and deductions for each pay period.

Is a pay stub the same as a paycheck?

No. A paycheck is the actual payment (paper check or direct deposit). A pay stub is the detailed document that explains how that payment amount was calculated — showing gross pay, all deductions, and the resulting net pay.

How long should I keep my pay stubs?

The IRS recommends keeping tax records for at least 3 years. Keep pay stubs for at least one year, then verify against your W-2. After reconciliation, store digitally or discard.

Can I make my own pay stub?

Yes! If you're self-employed, creating your own pay stubs is completely legal as long as the information accurately reflects your real income.

What's the difference between a pay stub and a W-2?

A pay stub shows one pay period; a W-2 summarizes the entire year. Pay stubs prove current income, while W-2s are required for tax filing.

Conclusion: Master Your Pay Stub, Master Your Finances

Now you know exactly what a pay stub is and how to read every section. This knowledge empowers you to catch payroll errors, provide confident proof of income to lenders and landlords, and understand where your hard-earned money goes every pay period.

Sources & References

- IRS Publication 15 (Circular E) — Employer's Tax Guide

- IRS Publication 15-T — Federal Income Tax Withholding Methods

- DOL — Fair Labor Standards Act

- DOL — Overtime Pay Requirements

- Social Security Administration — Contribution and Benefit Base

- IRS — Understanding Employment Taxes

- DOL — Recordkeeping Requirements Under FLSA

- IRS — How Long Should I Keep Records?

About David Chen

David is a CPA with 15 years of hands-on experience in payroll administration. He advises businesses of all sizes on tax compliance, employee classification, and payroll best practices.