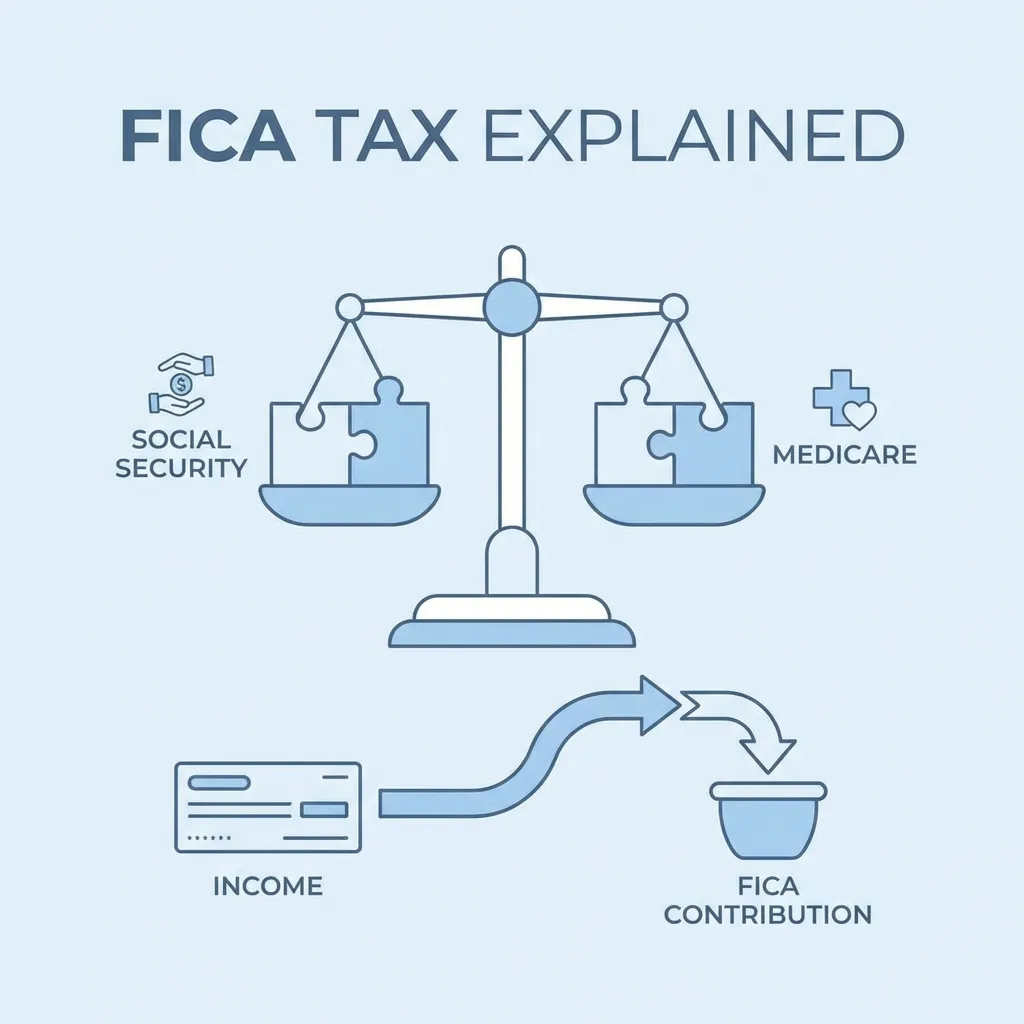

FICA Tax Explained: Social Security & Medicare Deductions Guide (2026)

FICA Tax Explained: Social Security & Medicare Deductions Guide (2026)

Every working American sees "FICA" on their pay stub — but most people have no idea what it stands for, how it's calculated, or where that money actually goes. If you've ever wondered why your paycheck has separate deductions for "Social Security" and "Medicare," you're looking at FICA in action.

In this comprehensive guide, we'll explain everything you need to know about FICA tax: what it is, how both components are calculated, who pays it, and why it matters for your financial planning.

What is FICA Tax?

FICA stands for the Federal Insurance Contributions Act, a law enacted in 1935 as part of President Roosevelt's New Deal. It established a mandatory payroll tax system to fund two critical social programs:

- Social Security (Old-Age, Survivors, and Disability Insurance — OASDI)

- Medicare (Hospital Insurance — HI)

Together, these two taxes combine to form what we call "FICA tax." According to the IRS, FICA tax is mandatory for virtually all employees and employers in the United States.

FICA at a Glance

| Component | Employee Rate | Employer Rate | Combined Rate | Annual Wage Limit |

|---|---|---|---|---|

| Social Security (OASDI) | 6.2% | 6.2% | 12.4% | $176,100 (2026) |

| Medicare (HI) | 1.45% | 1.45% | 2.9% | No limit |

| Additional Medicare | 0.9% | 0% | 0.9% | Over $200,000 |

| Total FICA | 7.65% | 7.65% | 15.3% | — |

Key Point: While you see 7.65% taken from your paycheck, your employer pays an equal 7.65% on your behalf — meaning the total FICA contribution on your earnings is actually 15.3%.

Social Security Tax (OASDI) — The Details

Social Security is the larger of the two FICA components. It funds retirement benefits for approximately 67 million Americans, plus disability benefits and survivor benefits for families of deceased workers.

Rate and Wage Base Limit

- Employee Rate: 6.2% of gross pay

- 2026 Wage Base Limit: $176,100 (adjusted annually for inflation)

- Maximum Annual Employee Contribution: $176,100 × 6.2% = $10,918.20

The wage base limit means Social Security tax only applies to the first $176,100 of your annual earnings. Every dollar above that threshold is exempt from Social Security tax (though still subject to Medicare tax).

How Social Security Tax Is Calculated

Standard Calculation:

Social Security Tax = Gross Pay × 6.2% (on earnings up to $176,100)

Bi-Weekly Example ($60,000 Annual Salary):

- Gross Pay per period: $2,307.69

- Social Security: $2,307.69 × 6.2% = $143.08

- Annual Total: $143.08 × 26 = $3,720.00

High-Income Example ($250,000 Annual Salary):

- Social Security on first $176,100: $176,100 × 6.2% = $10,918.20

- Social Security on remaining $73,900: $0 (above the cap)

- Total Annual Social Security: $10,918.20

The Wage Base Limit Through the Years

The Social Security wage base has increased steadily over time, adjusted by the SSA based on national average wages:

| Year | Wage Base Limit | Max Employee SS Tax |

|---|---|---|

| 2020 | $137,700 | $8,537.40 |

| 2022 | $147,000 | $9,114.00 |

| 2024 | $168,600 | $10,453.20 |

| 2025 | $172,800 | $10,713.60 |

| 2026 | $176,100 | $10,918.20 |

What Social Security Pays For

Your Social Security contributions fund:

- Retirement benefits: Monthly payments starting as early as age 62 (reduced) or at full retirement age (66-67)

- Disability Insurance (SSDI): Income replacement if you become unable to work due to disability

- Survivor benefits: Monthly payments to spouses, children, and dependents of deceased workers

Medicare Tax (HI) — The Details

Medicare tax — the smaller FICA component — funds Hospital Insurance (Part A) for Americans aged 65 and older, plus younger people with certain disabilities.

Rate and Limits

- Employee Rate: 1.45% of gross pay

- Wage Limit: None — Medicare applies to every dollar you earn, with no cap

- Additional Medicare Tax: 0.9% on earnings over $200,000 (single) or $250,000 (married filing jointly)

The Additional Medicare Tax was introduced by the Affordable Care Act in 2013 to provide additional funding for Medicare. Unlike regular Medicare tax, the employer does not match this 0.9% — only the employee pays it.

How Medicare Tax Is Calculated

Standard Calculation:

Medicare Tax = Gross Pay × 1.45%

Additional Medicare = (Total Income - $200,000) × 0.9% (if applicable)

Bi-Weekly Example ($60,000 Salary):

- Gross Pay: $2,307.69

- Medicare: $2,307.69 × 1.45% = $33.46

- Additional Medicare: $0 (income under $200,000)

High-Income Example ($300,000 Salary):

- Regular Medicare: $300,000 × 1.45% = $4,350.00

- Additional Medicare: ($300,000 - $200,000) × 0.9% = $900.00

- Total Annual Medicare: $5,250.00

What Medicare Pays For

Your Medicare contributions provide:

- Part A (Hospital Insurance): Inpatient hospital care, skilled nursing, hospice, and some home health care

- Parts B, C, D: Funded separately through premiums and general tax revenue (not through FICA)

FICA for Self-Employed Workers

If you're self-employed, you pay both the employee and employer portions of FICA — a combined rate of 15.3%. The IRS calls this Self-Employment Tax, and it's reported on Schedule SE of your tax return.

Self-Employment Tax Breakdown

| Component | Rate |

|---|---|

| Social Security (both halves) | 12.4% |

| Medicare (both halves) | 2.9% |

| Total Self-Employment Tax | 15.3% |

| Additional Medicare (if over $200K) | +0.9% |

The Self-Employment Tax Deduction

To offset the burden, the IRS allows self-employed individuals to:

- Deduct the employer-equivalent portion (7.65%) of self-employment tax from adjusted gross income

- Calculate SE tax on 92.35% of net self-employment earnings (not 100%)

Example ($100,000 Net Self-Employment Income):

- Taxable base: $100,000 × 92.35% = $92,350

- Social Security: $92,350 × 12.4% = $11,451.40

- Medicare: $92,350 × 2.9% = $2,678.15

- Total SE Tax: $14,129.55

- Deductible portion (half): $7,064.78

If you're self-employed and need to create professional pay stubs showing your FICA calculations, use our which handles the self-employment tax math automatically.

Who is Exempt from FICA?

While FICA is mandatory for most workers, the IRS recognizes limited exemptions:

| Exempt Group | Details |

|---|---|

| Certain religious groups | Members who have taken a vow of poverty or belong to recognized religious sects |

| Student workers | Students employed by the university where they study (under specific conditions) |

| Foreign government employees | Diplomats and other foreign government workers |

| Certain visa holders | F-1, J-1, M-1, and Q-1 visa holders (temporarily) |

| State/local government employees | Some who participate in qualifying public pension systems |

Note: These exemptions are narrow and very specific. The vast majority of workers — including part-time employees, contractors, and gig workers — must pay FICA.

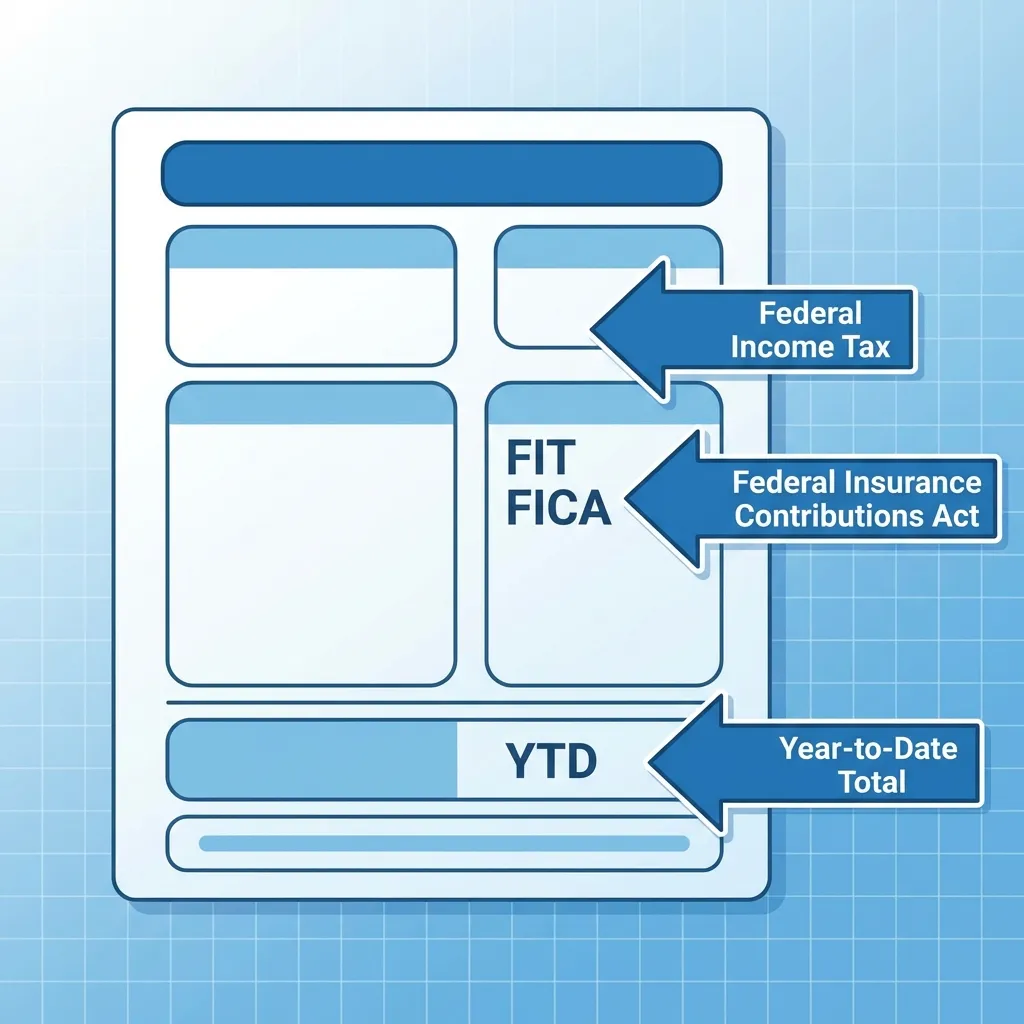

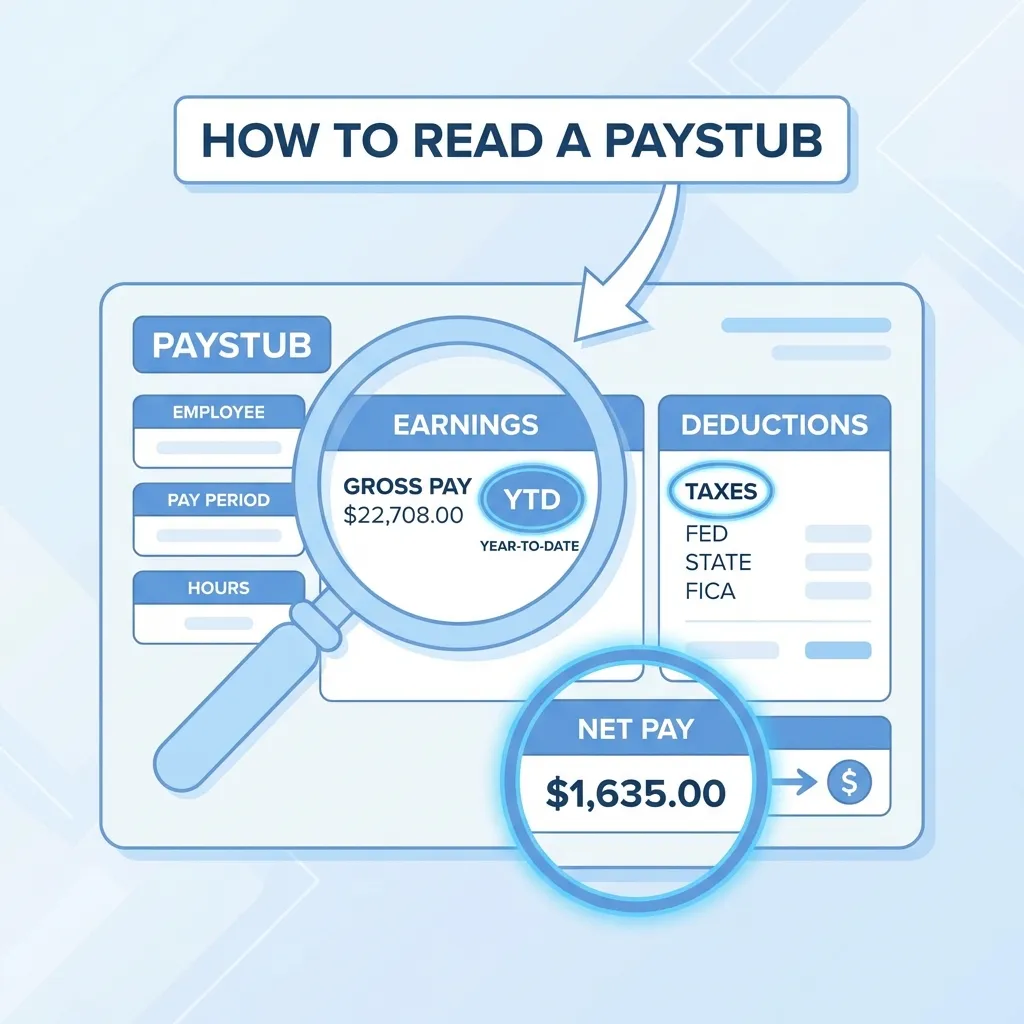

How FICA Appears on Your Pay Stub

Understanding how to find and verify FICA on your pay stub is essential for catching errors. FICA appears in the "Deductions" or "Taxes" section under various abbreviations:

Common Labels

| What You See | What It Means |

|---|---|

| FICA-SS | Social Security tax |

| OASDI | Old-Age, Survivors, and Disability Insurance (Social Security) |

| Soc Sec | Social Security |

| SS Tax | Social Security tax |

| FICA-Med | Medicare tax |

| Medicare or Med | Medicare tax |

| HI | Hospital Insurance (Medicare) |

| Add'l Med | Additional Medicare Tax (0.9%) |

How to Verify Your FICA Is Correct

Perform this quick check on every pay stub:

- ✅ Social Security = Gross Pay × 6.2% (should be exactly this, down to the penny)

- ✅ Medicare = Gross Pay × 1.45% (should be exactly this)

- ✅ Total FICA = Gross Pay × 7.65%

- ✅ YTD Social Security ≤ $10,918.20 (2026 maximum)

If any of these calculations don't match, there may be a payroll error. Contact your employer's HR or payroll department. For a deeper dive into all pay stub abbreviations, see our complete paystub reading guide.

FICA vs. Income Tax: Understanding the Difference

Many people confuse FICA with income tax. Here's how they differ:

| Feature | FICA Tax | Income Tax |

|---|---|---|

| Rate | Flat (7.65%) | Progressive (10-37%) |

| Purpose | Funds Social Security & Medicare | Funds general government |

| Calculation | Same % for everyone | Depends on income, filing status, deductions |

| Wage Limit | SS has $176,100 cap | No cap |

| Deductible | No (employee portion) | Reduced by deductions and credits |

| Employer Match | Yes (employer pays equal 7.65%) | No employer match |

For a complete breakdown of all paycheck deductions, see our understanding payroll taxes guide.

Frequently Asked Questions

Why is FICA tax mandatory?

FICA is mandatory because Social Security and Medicare are universal programs. The system works on a "pay-as-you-go" basis — current workers fund benefits for current retirees. Without mandatory participation, the programs couldn't function.

Can I opt out of FICA?

For the vast majority of workers, no. FICA is compulsory. The limited exemptions apply only to specific religious groups, certain foreign workers, and some government employees with qualifying pension plans.

Will I get my FICA money back?

Not directly as a refund, but your FICA contributions earn you "credits" toward future benefits:

- Social Security: You need 40 credits (approximately 10 years of work) to qualify for retirement benefits. Your benefit amount is calculated based on your highest 35 years of earnings.

- Medicare: You qualify for premium-free Part A with 40 credits.

- Disability: SSDI benefits are available if you become disabled and have sufficient work credits.

What if my employer withheld too much Social Security?

If you had multiple employers and the combined Social Security withholding exceeded the annual maximum ($10,918.20 in 2026), you can claim the excess as a credit on your tax return. If a single employer over-withheld, you must request a refund directly from that employer.

Does FICA apply to all income types?

FICA applies to employment income (wages, salaries, tips) and self-employment income. It does not apply to investment income (dividends, capital gains, interest), rental income, or pension/retirement distributions.

Conclusion

FICA tax is one of the most predictable and verifiable deductions on your pay stub. Understanding how Social Security (6.2%) and Medicare (1.45%) are calculated helps you:

- ✅ Verify paystub accuracy — catch payroll errors immediately

- ✅ Plan for retirement — understand what benefits you're earning

- ✅ Make informed financial decisions — know exactly where 7.65% of every paycheck goes

- ✅ Prepare for self-employment — understand the 15.3% self-employment tax

Key 2026 Numbers to Remember:

- Combined FICA Rate: 7.65% (employee) / 15.3% (total)

- Social Security Wage Base: $176,100

- Maximum SS Tax: $10,918.20

- Additional Medicare Threshold: $200,000 (single)

More guides: How to Read a Paystub • Payroll Taxes Guide • Gross Pay vs Net Pay

Sources & References

- IRS Topic 751 — Social Security and Medicare Withholding Rates

- Social Security Administration — Contribution and Benefit Base

- SSA — FICA & SECA Tax Rates

- IRS — Understanding Employment Taxes

- IRS Publication 15 (Circular E) — Employer's Tax Guide

- IRS — Self-Employment Tax

- IRS — Additional Medicare Tax

- IRS — Schedule SE (Form 1040)

About ValidPaystubs Editorial Team

Our editorial team consists of HR professionals and financial writers dedicated to providing accurate, up-to-date information on payroll and income verification.