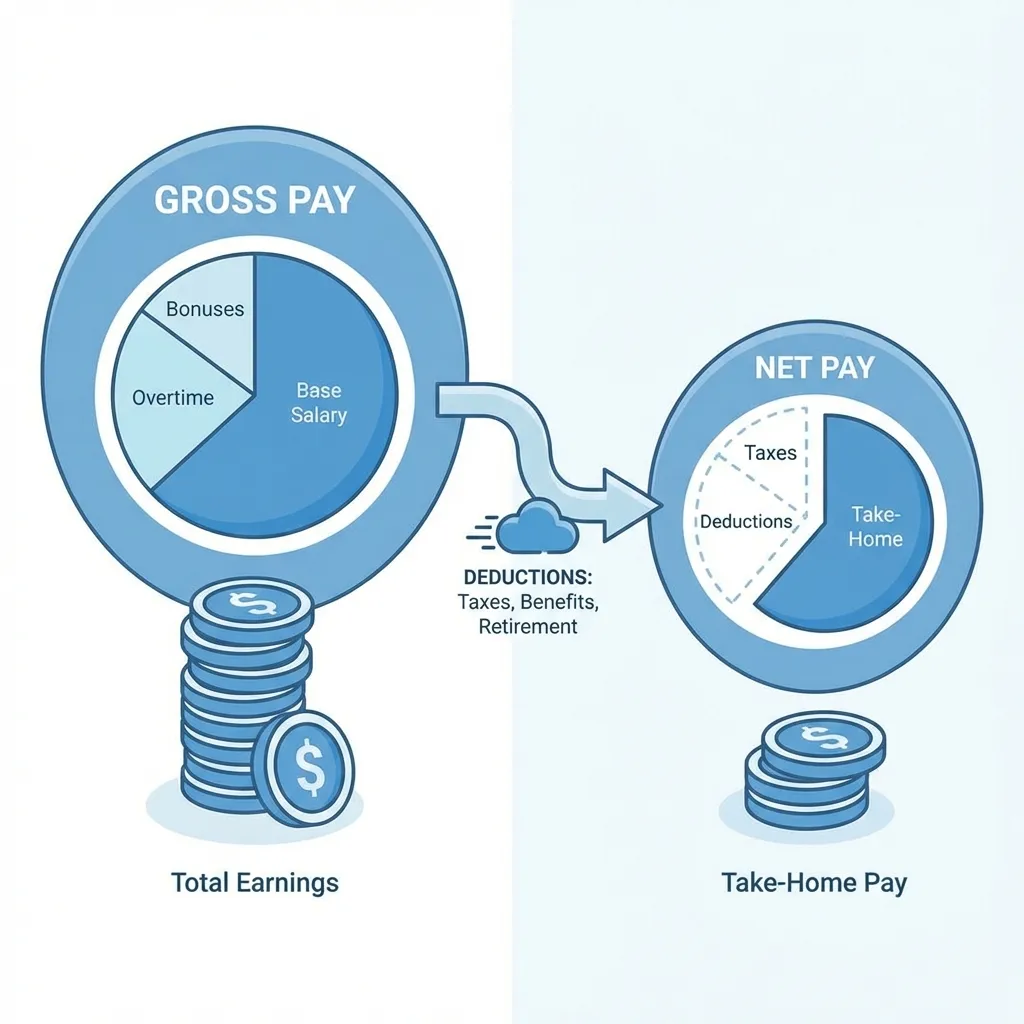

Gross Pay vs Net Pay: Complete Guide to Understanding Your Paycheck (2026)

Gross Pay vs Net Pay: Complete Guide to Understanding Your Paycheck (2026)

You got a job offer for $60,000 per year. You do some quick mental math — that's $5,000 per month, right? But when your first paycheck hits your bank account, you see something closer to $3,600. Where did $1,400 go?

The answer lies in the difference between gross pay and net pay — two numbers that appear on every pay stub and that fundamentally shape your financial life. Understanding this distinction is essential for budgeting, applying for loans, apartment hunting, and making informed career decisions.

What is Gross Pay?

Gross Pay is your total earnings before any taxes or deductions are subtracted. It's the "headline number" — the salary your employer agreed to pay you, or the total hours worked multiplied by your hourly rate.

Think of gross pay as the raw total of everything you earned during a pay period.

What's Included in Gross Pay

Gross pay encompasses more than just your base salary or hourly wages. According to the IRS, gross pay includes:

- Regular wages — Your base salary or hourly rate × hours worked

- Overtime pay — Time-and-a-half (1.5x) for hours over 40 per week under FLSA rules

- Commissions — Sales-based earnings

- Bonuses — Performance, signing, or holiday bonuses

- Tips — Reported tip income

- Holiday/vacation pay — Paid time off

Example — Hourly Worker:

| Earnings Type | Hours | Rate | Amount |

|---|---|---|---|

| Regular Pay | 80 | $25.00 | $2,000.00 |

| Overtime | 10 | $37.50 | $375.00 |

| Holiday Pay | 8 | $25.00 | $200.00 |

| Gross Pay | $2,575.00 |

Example — Salaried Worker:

| Calculation | Amount |

|---|---|

| Annual Salary | $75,000 |

| ÷ 26 pay periods (bi-weekly) | $2,884.62 |

| + Quarterly bonus ($2,000 ÷ 26) | $76.92 |

| Gross Pay | $2,961.54 |

What is Net Pay?

Net Pay is your take-home pay — the actual amount deposited into your bank account after all taxes, insurance premiums, retirement contributions, and other deductions have been subtracted. It's also called:

- Take-home pay

- After-tax income

- Disposable income

- "What actually hits your bank"

The Simple Formula:

Net Pay = Gross Pay - All Deductions

Net pay is always lower than gross pay. For most American workers, net pay is approximately 65-80% of gross pay, depending on income level, state of residence, and benefits elections.

How Deductions Transform Gross Pay Into Net Pay

The difference between gross and net pay comes from deductions — mandatory taxes and voluntary benefits. Here's a complete breakdown of everything that's subtracted:

Mandatory Tax Deductions (You Can't Avoid These)

| Deduction | Rate | 2026 Details |

|---|---|---|

| Federal Income Tax | 10-37% (progressive) | Based on IRS tax brackets and your W-4 |

| Social Security (OASDI) | 6.2% | On first $176,100 of earnings |

| Medicare | 1.45% | On all earnings, no cap |

| Additional Medicare | 0.9% | On earnings over $200,000 |

| State Income Tax | 0-13.3% | Varies by state; 9 states have no income tax |

| Local/City Tax | 0-3.9% | Only in some cities (NYC, Philadelphia, etc.) |

Voluntary Deductions (Benefits You Chose)

| Deduction | Typical Amount | Pre-Tax? |

|---|---|---|

| Health Insurance | $50-$500/paycheck | Yes (Section 125) |

| Dental/Vision | $10-$50/paycheck | Yes |

| 401(k) Traditional | 3-15% of gross | Yes |

| 401(k) Roth | 3-15% of gross | No (after-tax) |

| HSA Contributions | Up to $4,300/yr (individual) | Yes |

| FSA Contributions | Up to $3,200/yr | Yes |

| Life Insurance | $5-$30/paycheck | Partially |

| Disability Insurance | $10-$40/paycheck | Varies |

Other Possible Deductions

- Union dues — If you're in a labor union

- Wage garnishments — Court-ordered for child support, student loans, or debts

- Charitable contributions — If set up through payroll

- Parking/transit benefits — Pre-tax commuter benefits

Understanding Pre-Tax Deductions: When a deduction is "pre-tax," it reduces your taxable income. If you contribute $200 to a 401(k) from a $3,000 gross pay, you're taxed as if you earned $2,800 — saving you money on both income taxes and FICA taxes.

Real-World Example: The $75,000 Salary

Let's trace the complete journey from gross pay to net pay for a single filer earning $75,000/year in California, paid bi-weekly (26 pay periods), with standard benefits:

Step 1: Start with Gross Pay

$75,000 ÷ 26 = $2,884.62 per pay period

Step 2: Subtract Pre-Tax Deductions

| Pre-Tax Deduction | Amount |

|---|---|

| 401(k) — 6% | -$173.08 |

| Health Insurance | -$125.00 |

| HSA | -$82.69 |

| Taxable Income | $2,503.85 |

Step 3: Calculate and Subtract Taxes (on taxable income)

| Tax | Calculation | Amount |

|---|---|---|

| Federal Income Tax | Based on $65,100 taxable annually | -$301.47 |

| Social Security | $2,884.62 × 6.2% | -$178.85 |

| Medicare | $2,884.62 × 1.45% | -$41.83 |

| California State Tax | Based on CA brackets | -$117.50 |

| CA SDI | $2,884.62 × 1.1% | -$31.73 |

| Total Taxes | -$671.38 |

Step 4: Calculate Net Pay

| Line Item | Amount |

|---|---|

| Gross Pay | $2,884.62 |

| Pre-Tax Deductions | -$380.77 |

| Taxes | -$671.38 |

| Net Pay (Take Home) | $1,832.47 |

Result: From a $75,000 salary, this person takes home $1,832.47 per paycheck — approximately 63.5% of gross pay. The remaining 36.5% goes to taxes ($671) and benefits ($381).

How the Same Salary Differs by State

Where you live dramatically affects your net pay. Here's a comparison of the same $75,000 salary across different states (single filer, same benefits):

| State | State Tax Rate | Approx. Net Pay (Bi-Weekly) | Annual Take-Home |

|---|---|---|---|

| Texas (no income tax) | 0% | $1,950 | $50,700 |

| Florida (no income tax) | 0% | $1,950 | $50,700 |

| North Carolina (flat) | 4.5% | $1,885 | $49,010 |

| Illinois (flat) | 4.95% | $1,873 | $48,698 |

| New York | ~5.5% effective | $1,850 | $48,100 |

| California | ~6.5% effective + SDI | $1,832 | $47,644 |

| NYC Resident | ~5.5% + 3.5% city | $1,750 | $45,500 |

Key Insight: A person earning $75,000 in Texas takes home roughly $3,000+ more per year than the same person in California, and $5,200+ more than someone in New York City — just from state and local tax differences.

For state-specific pay stub details, see our state-by-state requirements guide.

Gross Pay vs Net Pay: When to Use Each

Understanding which number to use in different situations prevents costly mistakes:

Use GROSS PAY For:

| Situation | Why Gross? |

|---|---|

| Apartment applications | Landlords calculate income-to-rent ratio using gross |

| Mortgage applications | DTI ratio is based on gross income |

| Car loan applications | Lenders assess ability to pay using gross |

| Salary negotiations | Job offers are discussed in gross terms |

| W-2 reporting | W-2 Box 1 shows gross taxable wages |

| Tax bracket calculations | Federal brackets apply to gross adjusted income |

Use NET PAY For:

| Situation | Why Net? |

|---|---|

| Monthly budgeting | Budget based on what you actually receive |

| Emergency fund planning | Calculate 3-6 months of net expenses |

| Bank statement matching | Net pay should match your deposits |

| Spending decisions | You can only spend what hits your account |

| Paycheck verification | Confirm your deposit matches your stub |

How to Increase Your Net Pay (Without a Raise)

You can't change mandatory taxes, but you can optimize your deductions to maximize take-home pay:

1. Adjust Your W-4 Withholding

If you consistently get large tax refunds (over $500), you're over-withholding. Use the IRS Tax Withholding Estimator to adjust your W-4 and keep more money per paycheck.

2. Maximize Pre-Tax Contributions Strategically

While pre-tax contributions to a 401(k) reduce your net pay now, they also reduce your taxable income — meaning you pay less in taxes overall. Consider contributing at least enough to get your employer's full match (free money).

3. Use an HSA or FSA

If you have a high-deductible health plan, contributing to an HSA saves you money three ways: contributions are pre-tax, growth is tax-free, and withdrawals for medical expenses are tax-free.

4. Review Your Benefits Annually

During open enrollment, review whether you're paying for benefits you don't need (extra life insurance, double coverage, etc.). Dropping unnecessary coverage immediately increases net pay.

5. Move to a Lower-Tax State

While drastic, relocating from a high-tax state to a no-income-tax state can increase your annual take-home pay by $3,000-$7,000 on a $75,000 salary.

Frequently Asked Questions

Why is there such a big difference between gross and net pay?

Mandatory taxes (federal, state, FICA) typically reduce gross pay by 20-30%. Add voluntary deductions like health insurance and retirement contributions, and the total reduction can reach 30-40%.

Which number should I use for budgeting?

Always budget based on net pay — this is the actual money available for spending, saving, and bills.

Which number do lenders and landlords use?

Lenders and landlords use gross pay to calculate qualification ratios. A landlord checking the 3x rent rule uses your gross monthly income, not your net.

Can I increase my net pay without earning more?

Yes — by adjusting your W-4 withholding (if you're over-withholding), reducing unnecessary benefit deductions, or maximizing tax-advantaged accounts. See the strategies section above.

What percentage of gross pay is typical net pay?

For most American workers, net pay is approximately 65-80% of gross pay. Higher earners in high-tax states may see net pay as low as 55-60% of gross. Workers in no-income-tax states with minimal benefits may see 75-80%.

How do I verify my gross and net pay are correct?

Check your pay stub every pay period: verify that gross pay matches your rate × hours (or salary ÷ pay periods), that each tax deduction is the correct percentage, and that net pay = gross - all deductions. Your net pay should also match your bank deposit.

Conclusion

Understanding gross pay vs net pay is one of the most important financial literacy skills. Both numbers serve different purposes:

- Gross pay tells you what you earn and is used for applications and tax calculations

- Net pay tells you what you keep and is the foundation for budgeting

If you're self-employed and need to generate pay stubs showing accurate gross-to-net calculations with proper tax deductions, our handles all the math automatically using current 2026 tax tables for all 50 states.

More guides: How to Read a Paystub • FICA Tax Explained • Understanding Payroll Taxes

Sources & References

- IRS Publication 15 (Circular E) — Employer's Tax Guide

- IRS Publication 15-T — Federal Income Tax Withholding Methods

- Social Security Administration — Contribution and Benefit Base

- IRS Topic 751 — Social Security and Medicare Withholding Rates

- IRS — Tax Withholding Estimator

- DOL — Overtime Pay Requirements

- BLS — Usual Weekly Earnings of Wage and Salary Workers

About ValidPaystubs Editorial Team

Our editorial team consists of HR professionals and financial writers dedicated to providing accurate, up-to-date information on payroll and income verification.